Venture Capital: Legalized Gambling?

Explaining the Art of a Good Investment

Jan 10, 2024

Hello!

Thesis: Venture Capital is a large financial industry that plays a large role in the startup world, providing companies with key capital infusions they need to grow. Yet, they’ve essentially gotten rich through a form of legalized gambling—funding companies that have little to no chance of success in hopes of backing the next Unicorn.

Credit The Motley Fool

Ambrose Bierce once said, “The gambling known as business looks with austere disfavor upon the business known as gambling.”

Venture capital, like the stock market, is considered by some to be legalized gambling. Are these skeptics correct?

Venture Capital 101

First, before we start, I’ll give a little bit of my background, almost like you would in a court case, to establish why I may be able to provide some insights into the world of venture capital.

See, fully qualified to speak on the subject of venture capital.

(Yes I do actually have some experience in Venture Capital - see my LinkedIn or Bio if you’re truly concerned).

***Quick Note***

I’ll say the following insights aren’t going to necessarily be what you’ll see in a traditional introduction to venture capital like you would see for instance here, here, or here.

Let’s talk about what Venture Capital actually is and how it favors pretty much any background (I’ll use mine for reference).

Venture Capital is Sales.

The whole premise behind the world of Venture Capital is a transaction, a “buyer” and a “seller” –in a roundabout way.

Who is the seller in this instance? That’s where this gets interesting. To keep it simple I’ll use the following example: Say, for instance, a new software firm comes to a Venture Capital firm seeking money.

You would think naturally in this case, the company is the seller as they are trying to get the Venture Capital firm to “buy” into their idea. You wouldn’t be wrong, but you wouldn’t be entirely right.

In fact, both parties could be both parts of the transaction, the buyer AND the seller.

As said above, the company is a seller as they are trying to get the Venture Capital firm to buy into their idea (harder than you think but I’ll talk specifically about that further down).

The company is also a buyer in the way they are trying to buy the Venture Capital’s cash. They want their money. What are they giving up to get this cash? The most common approach in this type of transaction is for the company to trade a piece of equity (ownership in their company) to the Venture Capital firm in return for the Venture Capital firm’s cash.

But is cash the only thing they’re buying? Often, no. Depending on the Venture Capital firm, companies they own a portion of (called portfolio companies) also receive considerable “intangible” resources. Examples could be inter-industry connections (Venture Capital firms are often specialized leading them to know many key players in the industry), operational support resources (resources on how to go about running a business), and more.

Okay, but how is the Venture Capital firm a buyer and seller in this circumstance?

The Venture Capital firm is buying a piece of that company in the hopes that the company will grow and develop and eventually, the Venture Capital company can sell its equity and make money.

Selling is a little more difficult. For competitive companies, many different entities are trying to get a piece of the company (and hopefully a piece of future reward), so many times the Venture Capital company is required to sell itself to the company, essentially answering the common question of “why do you need us as opposed to someone else?”.

In addition, Venture Capital companies also sell their cash and valuation (the amount of money they estimate the company is worth - the company wants it to be higher so they are worth more and the Venture Capital firm has to buy fewer shares for the same amount - less of the company) for more favorable terms of deal structure from the company in order to be best suited for the future (for more information: term sheets).

Venture Capital is Entrepreneurship.

Someone once said to me that working in Venture Capital is the best and most efficient way to get your MBA (for practical reasons I have to note that you won’t actually end up with an MBA from working in Venture Capital, just extremely practical business administration experience).

I think that’s a sound way to look at it. From a Venture Capital perspective, you’re able to look at thousands of different businesses every year and pick the ones you think are the “best” to look at further.

How do you determine what is the best business?

This process is an art, not a science (although many people claim it can be automated in a way that makes it a sure thing - to this I say, where are your 100% returns every year for the next 30 years?). It’s why people get paid extremely large amounts of money for what they do.

Every good fund has a criteria: a general set of specifications/guidelines they invest with. For example, some of these can be company size, industry, amount of revenue, founding date, location, etc.

As a Venture Capitalist, you’ll look at thousands of companies a year. Of that, let’s assume at least 10 meet your initial criteria screen (although if your fund has a broader scope you might have hundreds or thousands). How then, do you identify what is the best business of the companies that already meet your general specifications?

This is where experience, knowledge, and gut come into play. At this point you start to look at more qualitative measures, for instance, how the management team runs their company, what backgrounds the management team has, how the industry in their geography is situated for their business to exploit, etc.

This is where you’re able to learn about how to run and/or look for a successful business (mainly about what a successful business does not look like). Doing thousands of these repetitions yearly, hopefully you pick up a thing or two about how to start a business and run one as an entrepreneur in your fund’s specific field.

Venture Capital is Research.

Say your fund’s specific directive is energy companies, for instance, and it’s your first day on the job. Your boss says that they expect 3 interesting companies by next week. How do you go about finding those companies?

Let’s even take one step back. As you start on this journey of finding interesting companies, maybe you realize you don’t know much about energy, let alone companies that deal with it. What do you do then?

Read.

Such an underrated skill. I’m convinced Venture Capital interviews should include one of those kindergarten Reading for Comprehension tests.

I’d say that during my time in Venture Capital, I’ve read around 100-1000 pages of information on companies, markets, institutions, technology, trends, politics, regulation, etc. every week.

Seems like a lot, but when you’re constantly flipping from business to business, you’re going to have to be able to get knowledgeable about spaces extremely quickly.

Venture Capital is Studying

Venture Capital investing can be seen as a series of tests. Each investment you make, each company you look at, and each conversation you have is a test to see if you’re a good investor worthy of doing business with.

Conversely, each conversation companies have, each fund they apply to, and each customer they serve is a test to see if their company provides quality products/services and is worthy of investment.

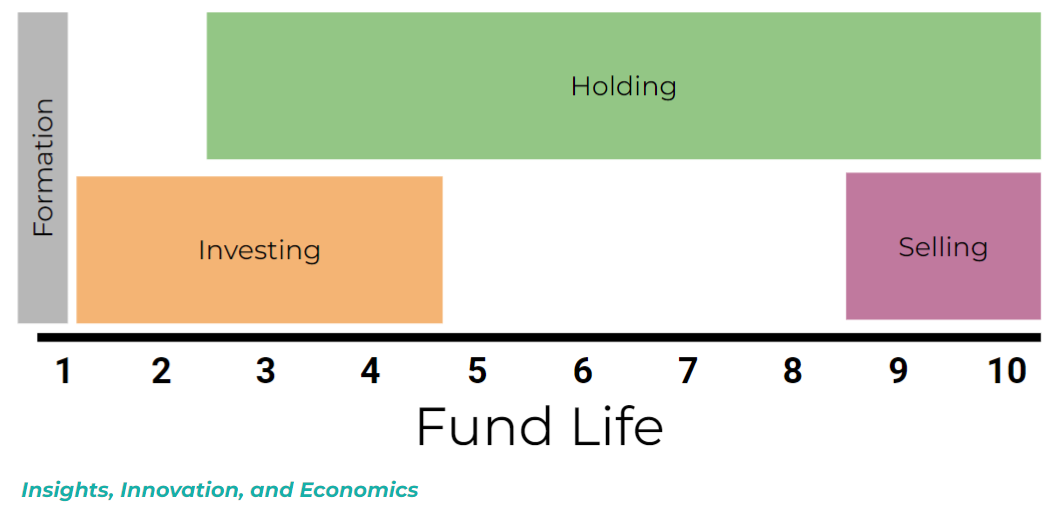

As a Venture Capitalist, when studying what companies to potentially invest in, a major factor in consideration is risk, primarily concerning fund lifecycle. Ideally, you would like all companies to be able to pay you back for your investment, but you have to be even more specific than that.

Most Venture Capital firms have investment timelines of around 3-7 years from the time they invest to the time they need to sell that investment and return the funds to their investors. So, in addition to companies having inherent risk, you need to find those that have the highest likelihood of paying you back within your necessary time period.

In addition, Venture Capital isn’t an industry for procrastinators. As a company looking to get funding, you have to constantly be on your game, ruthlessly competing for funding. As a Venture Capital firm, when companies come to you, you can’t sit on them for long (if at all) because someone else will swoop in and give them funding.

Credit: Inspire Uplift

Now that I’ve given you a little of my background and how it relates to Venture Capital, let me introduce you to the most sacred concept in Venture Capital, the Unicorn.

Here’s an excerpt from Encyclopedia Britannica on Unicorns:

The Appropriate Response: Wow! Thank you for giving me a very educational paragraph on the history of Unicorns, I learned so much! But why do I care?

There’s an entire industry built on them (hint: Venture Capital).

In Venture Capital, everyone strives to find a Unicorn.

As silly as that sounds, it’s true. Except in this case, a Unicorn is the term used for the next billion-dollar company. Amazon, Apple, Microsoft, these big companies you hear about constantly in the news are Venture Capital Unicorns. Some fund somewhere “caught” them, meaning they were able to invest early and reap incredible results.

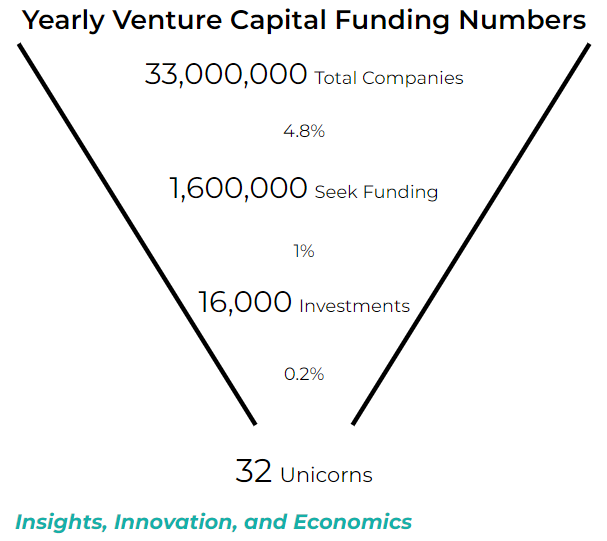

Let’s talk statistics for a moment.

Source Credit Statista, a16z

Dismal right? Each company that seeks funding from the United States every year has a 1 in 50,000 chance of becoming the next Unicorn. Even from a Venture Capital perspective, each company you actually invest in only has a 1 in 500 chance of becoming the next Unicorn.

So why do Venture Capital funds do it?

Money.

Specifically, fees and returns. In general, most funds operate on a “2 and 20” monetary structure where they receive 2% of the overall fund amount every year as a management fee - a fee to fund the day-to-day operations of investing and managing your portfolio. In addition, most funds also receive 20% of the money they return above the initial fund amount when the fund is finished.

For instance, consider a 10-year Venture Capital fund that invests in Google at $1M for its entire fund on the first day and holds the equity for 10 years then sells after 10 years for $10M. The Venture Capital company would receive $20,000 every year as a management fee. In addition, after selling their portion of Google, the investors would receive their initial investment of $1M + 80% of the other money ($9M * 80% = $7.2M), and the fund would receive 20% of the $9M (or $1.8M). In total, the investors would invest $1M and receive $8.2M in 10 years (pretty great return) and the fund would invest $0 and receive $2M over the 10 years.

Okay, so we’ve seen the stats on Venture Capital, and, to be honest, the average outcome is mediocre, but the payout is fantastic if you’re able to get it. High risk, high reward. Sound familiar?

Thesis: Venture Capital is a large financial industry that plays a large role in the startup world, providing companies with key capital infusions they need to grow. Yet, they’ve essentially gotten rich through a form of legalized gambling—funding companies that have little to no chance of success in hopes of backing the next Unicorn.

Anywho, that’s all for today.

-Drew Jackson

Disclaimer:

The views expressed in this blog are my own and do not represent the views of any companies I currently work for or have previously worked for. This blog does not contain financial advice - it is for informational and educational purposes only. Investing contains risks and readers should conduct their own due diligence and/or consult a financial advisor before making any investment decisions. This blog has not been sponsored or endorsed by any companies mentioned.