Unlocking Earnings: Strategies for Capturing Value from Innovation

Capturing Created Value is Difficult, or is it?

Feb 07, 2024

Hello!

Thesis: Innovation, from a company’s perspective, requires two complementary processes, first, that you’re creating value for your consumer, and second, that the company can capture some of that value created as profits. Companies are very good at the first part (you wouldn’t need a company if they didn’t make your life better in some way). Unfortunately, many times companies don’t have a strategy for capturing the value they create as profits, losing out on key profit streams.

If you haven’t read my Introduction to Economics Post, I’d highly recommend it before reading this article as some of the terminology can be difficult to understand.

William Brody, a 20th-century scientist once said:

The economy is built on the back of successful innovation.

Anywho, that’s all for today.

-Drew Jackson

If only it was that easy.

Well, it can be with the right strategy to capture value from your innovation.

Credit Deskera

Step 1: Create Value for Your Customer

Creating value is traditionally the step that most people understand and can competently complete.

Creating value for your customers means providing them with a product or service with the idea that they are better off after the transaction. To put it simply, the perceived benefit the consumer gets from your product is larger than the price you charge for your product.

Perceived benefit. That’s kind of vague language, what does that actually mean?

Perceived benefit can be most easily thought of as a marketing term. It means the customer’s evaluation of a product or service and its ability to meet their needs and expectations. In other words, it’s the benefit the customer thinks they will get from purchasing your product or service. The key word there is “thinks”.

The whole industry of marketing is there to convince you to increase your perceived benefit of products and services, because if your perceived benefit is greater than the price you are more likely to purchase the product or service.

Unfortunately, perceived value often doesn’t always equate to actual value. Consider the example of an impulse purchase you instantly regret, the perceived value is high but the actual value is quite low. Conversely consider eating a hamburger when you haven’t eaten all day. The perceived value is high but the actual value is even higher.

How do you know what is valuable to your customer?

Ironically this is the easy part. The market tells you. If consumers buy your product, it is creating value for them at that price. If consumers don’t buy your product, it means your product isn’t creating value for them at that price.

So, you need to understand your customer. What problems do you have? How important are those problems for them? Are you providing a solution that leaves them better off after purchasing?

Many startup companies don’t understand their customers. They see a problem and design what they think is the “solution” to it, yet many times that solution isn’t what the customers need for one reason or another, so they fail, or better yet, the customers didn’t see that problem as a problem and didn’t even need a solution for it.

To create value for a customer, you need to provide value and benefit in their life. This is where innovation comes in. Many good businesses are created off of these concepts, innovate then create a product that creates value for your customer.

Credit Epicurious

Step 2: Value Capture

Once you create value for your customer are you done?

You can be, but that’s not the economically sound answer.

Let’s say you are a restaurant that sells hamburgers. Your customers get $15 in total benefit from eating one of your hamburgers. Each burger costs $10, so your customers get a net benefit of $5 for each burger.

One of your research and development projects creates a new hamburger that has 100 fewer calories per burger. You make this burger the star of the show at your restaurant, so now everyone comes in to buy one. Your customers now get $20 in total benefits from eating one of these burgers. Each burger still costs them $10, so your customers now get a net benefit of $10 for each burger.

In this scenario, you created $5 of value for each customer ($20 - $15), but $0 of that value was captured as increased profit for your business through price.

Yet, did you fail to capture value?

Not necessarily. There are two different ways to capture value, first, through increased price, and second, through increased quantity.

When considering profit (captured value) for a firm, the simple equation is price * quantity - costs.

So, in our example above, if the normal scenario had 10 customers, meaning you netted $50 before costs, and the second scenario meant you attracted 5 more customers, you netted $75 before costs.

So, on paper, you captured more value from innovation.

Consider the alternative where you increased the price by $2 per burger, but kept the same amount of customers. This would mean you would net $70 before costs, capturing more value from before, but this time the value is captured from the same customers, not more customers.

This simple way of thinking about value creation and capture is a good starting place if you’re new to the subject.

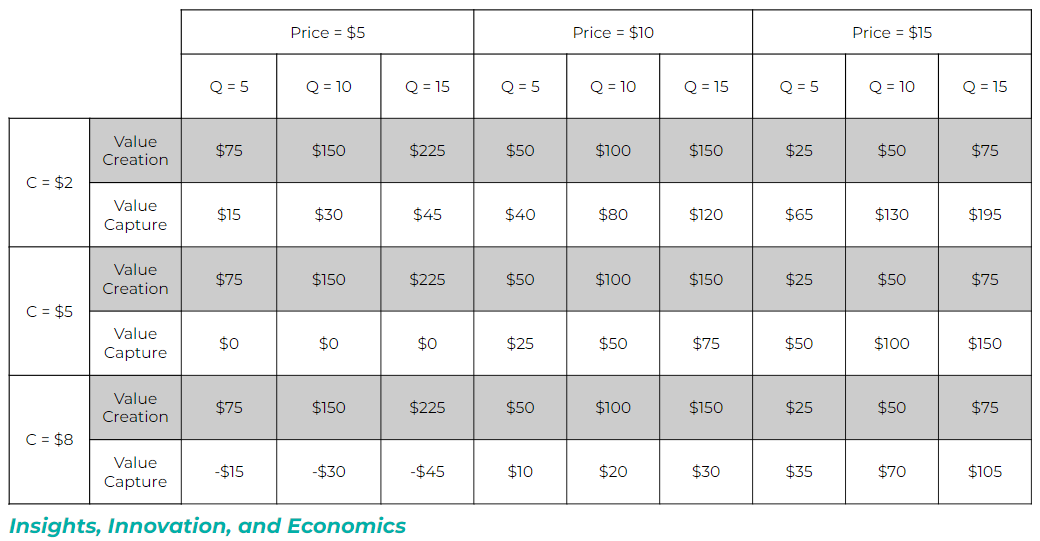

When you factor in costs, value creation and value capture become a little more difficult. If we assume that through innovation, your benefit to the customer goes up (not always true), let’s assume from $15 to $20, price can go up or down ($10 or $5 or $15), quantity can go from 5 to 10 or 15, and costs can go from $2 to $5 to $8, you have the following matrix of options:

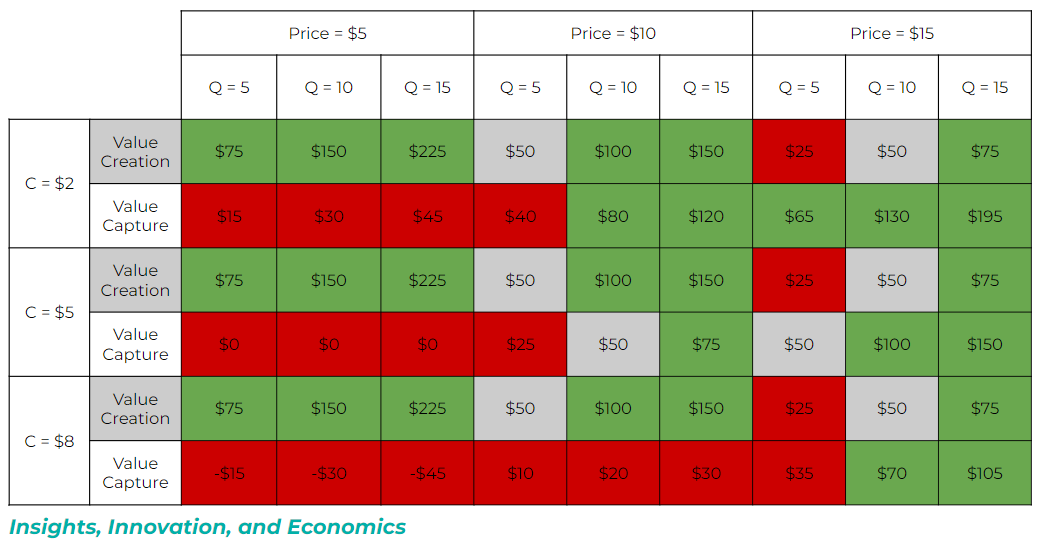

In this scenario, our current value creation is $50 ($15 benefit - $10 price * 10 quantity), and our value captured is $50 ($10 price - $5 cost * 10 quantity). Now, I’ll attach the same chart with the scenarios in which the higher or lower numbers are highlighted in green (good) or red (bad).

As you can see, adding in costs makes our example much more complicated. But, it does showcase some trends. In scenarios where the price goes down, the firm struggles to capture value (no matter the cost), but the value for the consumer is massive.

When the price stays the same, the value created for the consumer still increases, and in some scenarios, with lower costs or increased quantity, the firm can capture more value, but when costs go up, the firm still struggles to capture value.

And lastly, when the price goes up, we struggle to create more value for the consumer, but the firm almost always can capture more value.

Key Takeaways about Value Capture

Through innovation, if benefits go up, for the firm to capture value in some way, the price has to increase, the cost has to decrease, or the quantity has to increase.

Strategies for Capturing Value

Now that I’ve discussed how to go about capturing value (increase price, decrease cost, or increase quantity), what strategies do companies employ to actually capture value in the real world?

Credit PCMag

Case Study #1: Netflix

Netflixed revolutionized the entertainment industry by popularizing streaming services. They created value for customers by offering a vast library of on-demand content right at your fingertips. In addition, Netflix was able to capture value through its subscription-based business model, attracting millions of subscribers and capturing billions of dollars in income every year.

Netflix created value and was able to capture it successfully.

Credit Mashable

Case Study #2: Uber

Uber figured out how to create massive amounts of value for car drivers and passengers. For car drivers, Uber gave them a method to use their existing vehicles to create a source of flexible income. For passengers, Uber gave them a flexible ride-sharing service to get from A to B at relatively low costs.

In this case, Uber has struggled to capture value from this scenario as they have increased benefits and increased quantity, but costs are still high and prices are still low (to incentivize consumer adoption).

Uber created value but has failed to capture it, wasting billions of dollars in the process.

Creating Value & Capturing Value

To conclude, creating value for your customer is extremely important, and why the whole concept of innovation exists. Yet, failing to capture some of that value as profit is senseless, costly, and time-consuming.

Anywho, that’s all for today.

-Drew Jackson

Disclaimer:

The views expressed in this blog are my own and do not represent the views of any companies I currently work for or have previously worked for. This blog does not contain financial advice - it is for informational and educational purposes only. Investing contains risks and readers should conduct their own due diligence and/or consult a financial advisor before making any investment decisions. This blog has not been sponsored or endorsed by any companies mentioned.

brainwaves.me@gmail.com

brainwaves.me@gmail.com