Economics of ESG

Breaking ESG Down to the Basics

Aug 7, 2024

Hello!

Welcome to the Insights, Innovation, and Economics blog. If you’re new here, feel free to read my general Introduction to the Blog to understand more about the blog. If you’re returning, thank you, and hope you have a great read!

Thesis: ESG has been a popular buzzword in the business community, yet the investment prospects and other prominent statements aren’t always economically sound. Investors, managers, employees, and customers should understand the critical economics behind their support, or lack thereof, of ESG-focused companies or initiatives.

If you’re new here, please consider subscribing :)

Credit Buro Happold

ESG

ESG stands for environmental, social, and governance. I’ve you’ve been anywhere near the business world the last couple of years, you’ve probably heard about ESG.

Deloitte explains ESG with the following:

But what do the ESG pillars contain?

Environmental:

- Emissions such as greenhouse gases

- Resources the company uses, such as recycled materials in its production processes

- Companies should be good users of water resources

- Companies could report on positive sustainability impacts they are doing

Social:

- Employee development and labor processes

- Companies should make sure they report on safety and quality liabilities

- Supply chain labor, standards, and sourcing concerns

- Reporting on the accessibility of their products/services

Governance:

- Shareholders rights

- Board diversity

- Executive compensation and ESG performance benefits

- Corporate behavior practices such as anti-competitive or corruption

ESG is important when it comes to investing. See, the goal of ESG is to capture major non-financial risks and opportunities a company has.

This dates back to the early 2000s when United Nations officials began pressuring the finance industry to incorporate ESG into their processes. The United Nation’s advisors argued that investors’ fiduciary responsibilities should include the use of ESG factors in their financial analyses. ESG considerations could protect investments by avoiding risks associated with climate change, worker disputes, human rights issues, and poor corporate governance.

This began the ESG movement and the field of ESG investing.

Credit Harvard Business Review

ESG Economics

The economics underlying common ESG claims are often misconstrued. This can create a false sense of fact, urgency, or an incorrect investment thesis, all of which can be harmful.

For instance, people claim that ESG risks affect the cost of capital. This isn’t necessarily true as diversified investing removes idiosyncratic ESG risks (risks specific to that company only). This leaves only market-wide ESG risks–which tend to be global ESG risks.

Concerning ESG risk baked into company valuation, many companies include ESG risks in the discount rate when valuing cash flows. This means that including the ESG risks would decrease the value of the company since there is more likelihood of diminished returns or bankruptcy. Put another way, the thought is that, for most companies, ESG factors only provide further risks, with very minimal, if any, returns.

Using the discount rate to include ESG factors is incorrect, however. economics and finance tell us that the discount rate is only affected by market risks, not company-specific risks, so instead the numerator–the cash flows–should be adjusted for additional ESG risk.

Many investors claim that ESG concerns enhance shareholder value, meaning better ESG companies will have superior returns. Yet this isn’t the case. If ESG enhances shareholder value and this is known, the market would already have priced this in, leading to normal returns. Put another way, if the company has high ESG performance, the price to buy that company would be increased because of it, meaning returns would be normal.

Building on this, ESG factors may lead to superior returns if these factors are unanticipated. If they are anticipated, the price will increase to reflect them. For instance, if we had 2 of the same company where one had anticipated ESG factors and one had unanticipated ESG factors. The first company would start at $15 per share (as ESG factors are already priced in) and the second would start at $10. When both perform well, the stock price increases to $20. In one case, this was anticipated, leading to lower returns (similar to the returns of other stocks). In the other case, ESG factors weren’t anticipated, leading to higher returns since they weren’t already priced into the stock.

In equilibrium, there is no mispricing in the market as investors fully recognize the true value of ESG factors. In the market, stocks with high ESG factors may lead to lower returns as they hedge against government action on climate change or as investors have a taste for these stocks, artificially increasing the price and driving returns down.

Building on this, in equilibrium, investor returns equal the cost of capital (the amount of risk taken). This follows the saying “High risk, high return; low risk, low return”. If ESG factors lower the cost of capital, they must lead to lower returns. Yet, some ESG advocates claim that high ESG scores lower the risk of a company but increase shareholder returns. If you have lower risk, then it’s impossible in an equilibrium market to have high returns that follow.

Consider another common fad, the concept that more ESG is always better. That isn’t always the case. Like any other investment, ESG will experience diminishing returns–meaning that more ESG will produce less and less returns as the quantity of ESG continues to increase. In addition, the proponents of more ESG don’t factor in trade-offs/opportunity costs.

Another trend in ESG is linking executive performance to ESG targets. However, this doesn’t necessarily work as well with ESG factors as it does with other financial targets. Instead of trying to increase your revenue, an easy goal to measure, companies are trying to quantify qualitative targets. For instance, how do you quantify creating a more inclusive atmosphere? This leads executives to have surface-level ESG targets, targets that can sometimes detract from other company goals such as increased financial performance, customer penetration, or supply chain improvements. These goals rarely capture the true essence of ESG concerns.

Credit Consultancy Asia

ESG Investing

ESG investing is a methodology to screen investments based on corporate policies and to encourage companies to act responsibly.

What do investors look for when doing ESG investing?

Investopedia cites the following list of characteristics ESG investors could consider:

What are ESG funds?

There are a variety of ESG-specific funds including mutual funds, ETFs, and more. These funds follow ESG investing strategies–meaning they invest in the best ESG companies (usually based on a scoring ranking of some kind).

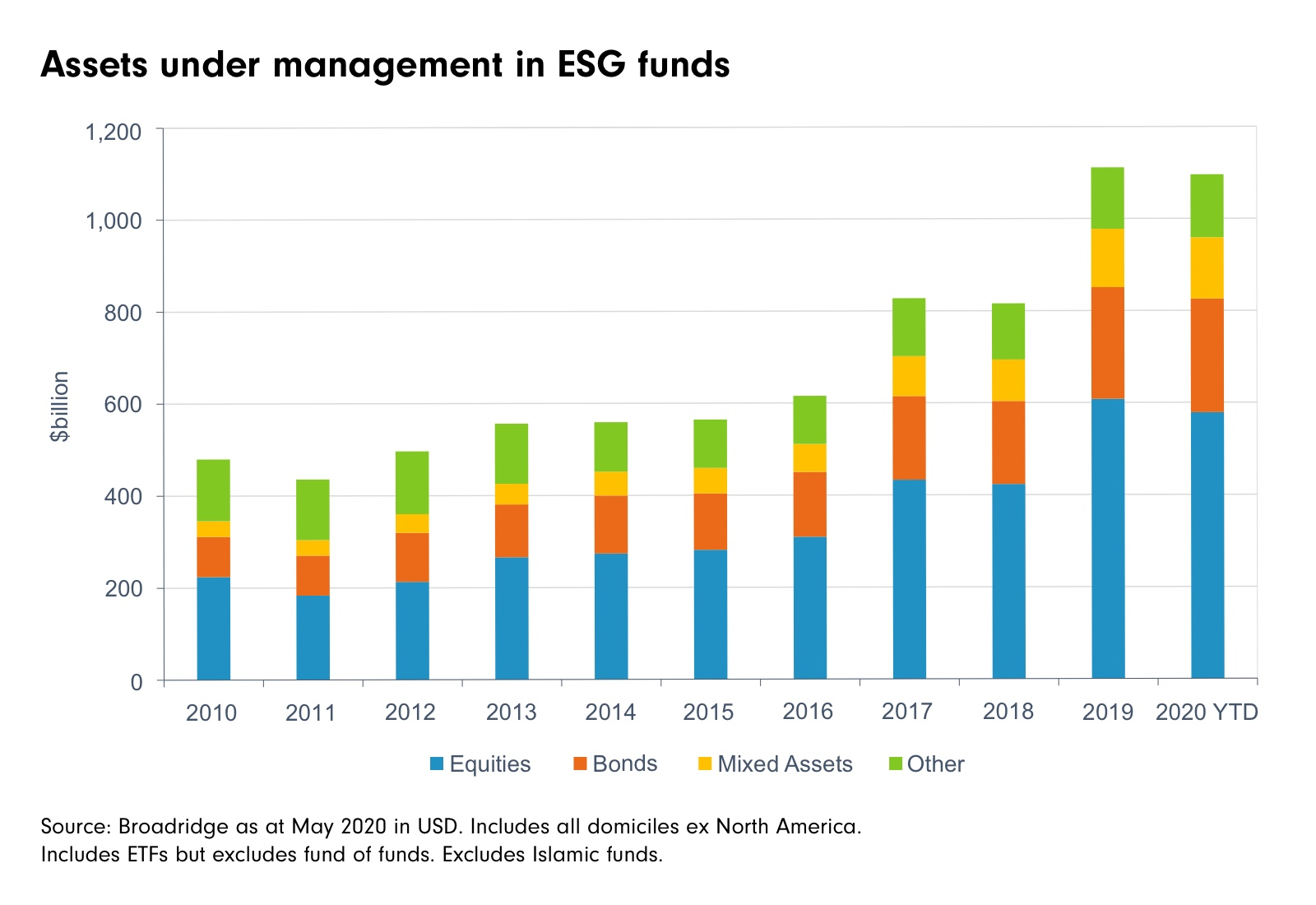

Here’s a graph from Fidelity UAE showing the number of assets under management (how much money a portfolio has) of all of the different ESG funds out there:

Why do people do ESG investing?

ESG investing can help individuals and portfolios avoid holding companies engaged in risky or unethical practices which can prevent bad press or pushback from limited partners.

Ultimately, the goal of ESG investing is to make money by investing in companies that have sustainable and ethical business practices. But, do these companies produce adequate returns?

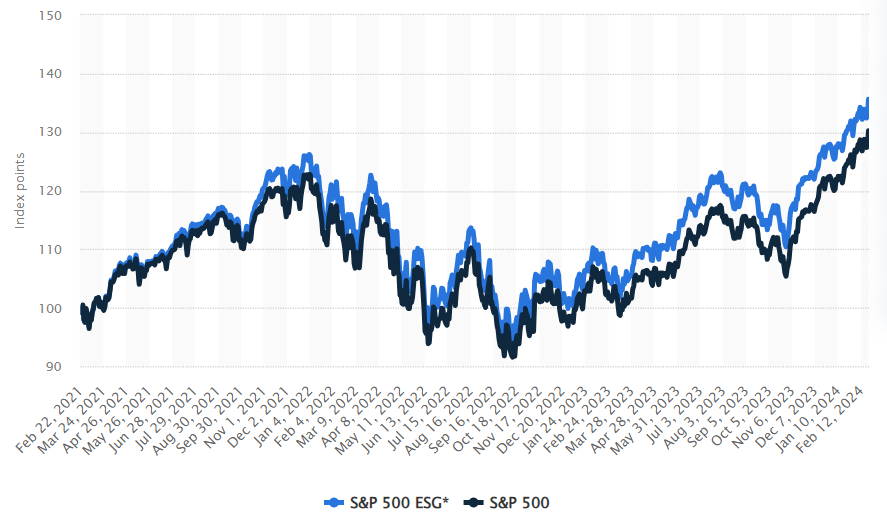

Here is a graph from Statista comparing the S&P 500 index vs. the S&P 500 ESG index from 2021 through 2024:

As you can see, since 2021, the ESG-specific index has slightly outperformed the total index.

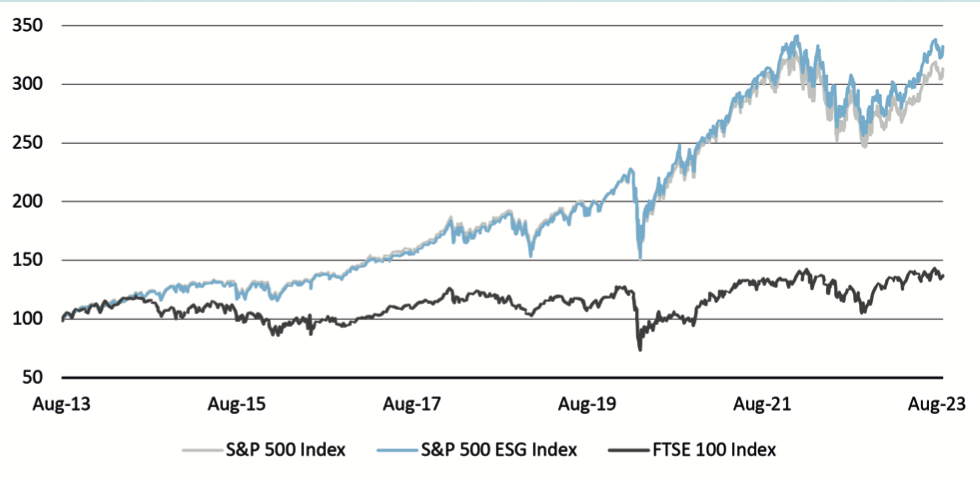

Taking a longer viewpoint, comparing the S&P 500 index vs. the S&P 500 ESG index vs. the FTSE 100 index (the United Kingdom’s version of the S&P 500) from 2013 to 2023:

If you look closely for the gray line signaling the general S&P 500 index, you’ll see that ESG funds have not significantly outperformed the normal S&P 500 index, but they haven’t underperformed either.

So what sets them apart from traditional funds?

On a returns basis, nothing it seems. However, in this new age of social issues awareness, an ESG fund may make it easier to market your fund and attract investors who are conscious of these issues.

Credit The Australian

Do ESG Considerations Work

ESG critics cite that the data isn’t great. It’s unsure which asset will outperform or underperform because of climate change. In addition, it’s unsure the timeline in which these performances will occur.

In addition, critics cite that commonly used ESG rates measure the impact of the changing world on a company’s profits and losses, not the reverse. These ratings don’t measure the company’s impact on the Earth and society, arguably a more important metric.

Unfortunately, everything on Wall Street boils down to shareholder returns. ESG issues are often presented as environmental, social, and governance aspirations from companies, yet the real goal is to identify conditions that could cause a negative impact on the value of the investment.

Furthermore, the goal of most ESG funds is to make an impact on the world through ESG concerns. However, it’s virtually impossible for ESG-motivated investors to increase the ESG-related outputs of a publicly traded corporation by purchasing their stock–unless, of course, you purchase enough to become an activist investor.

Yet, maybe the most important backlash for ESG concerns is that ESG concerns don’t provide enough incentive to truly change corporate behavior in a meaningful way. For instance, it’s unreasonable to expect corporate executives to put public interests ahead of private interests when tradeoffs are present (for instance, choosing to use more expensive recycled plastic instead of cheaper, brand-new plastic). These critics argue that although ESG concerns are a step in the right direction, incentives need to be better aligned between private profits and social welfare.

Ultimately, it’s up to you to decide where you stand concerning ESG measures. You may think it’s a much-needed step in the right direction, you may think ESG concerns are decent but nowhere near what is needed to enact change in the market, or you may think ESG concerns aren’t effective or needed.

To conclude, I’ll end with this quote by the famous explorer, Robert Swan:

Anywho, that’s all for today.

-Drew Jackson

I'll be back in your inbox on Wednesday

Disclaimer:

The views expressed in this blog are my own and do not represent the views of any companies I currently work for or have previously worked for. This blog does not contain financial advice - it is for informational and educational purposes only. Investing contains risks and readers should conduct their own due diligence and/or consult a financial advisor before making any investment decisions. This blog has not been sponsored or endorsed by any companies mentioned.

brainwaves.me@gmail.com

brainwaves.me@gmail.com